What Prava Solves

Traditional online checkout requires manual user input. AI apps can help with search and recommendation, but they can’t complete payments without:- Secure access to card credentials

- Verified user intent

- Trust between agents and merchants

- A standard way to deliver payment payloads

Developer Mental Model

Think of Prava as a programmable payment proxy. Instead of your AI agent handling raw credit card numbers (which creates massive compliance and security risks), it handles Intents—permissions to spend.- The Agent requests permission to buy a specific thing.

- The User grants permission via their device (Passkey).

- Prava exchanges that permission with the Card Network for a one-time, merchant-specific credential.

- The Agent uses that ephemeral credential to complete the checkout.

System Architecture

1. The Trust Layer (Identity)

Every AI agent interacting with merchants must be identifiable. Prava issues the agent a secure identity, enabling merchants to validate who is making the request. This establishes a chain of trust:User -> Agent -> Prava -> Merchant.

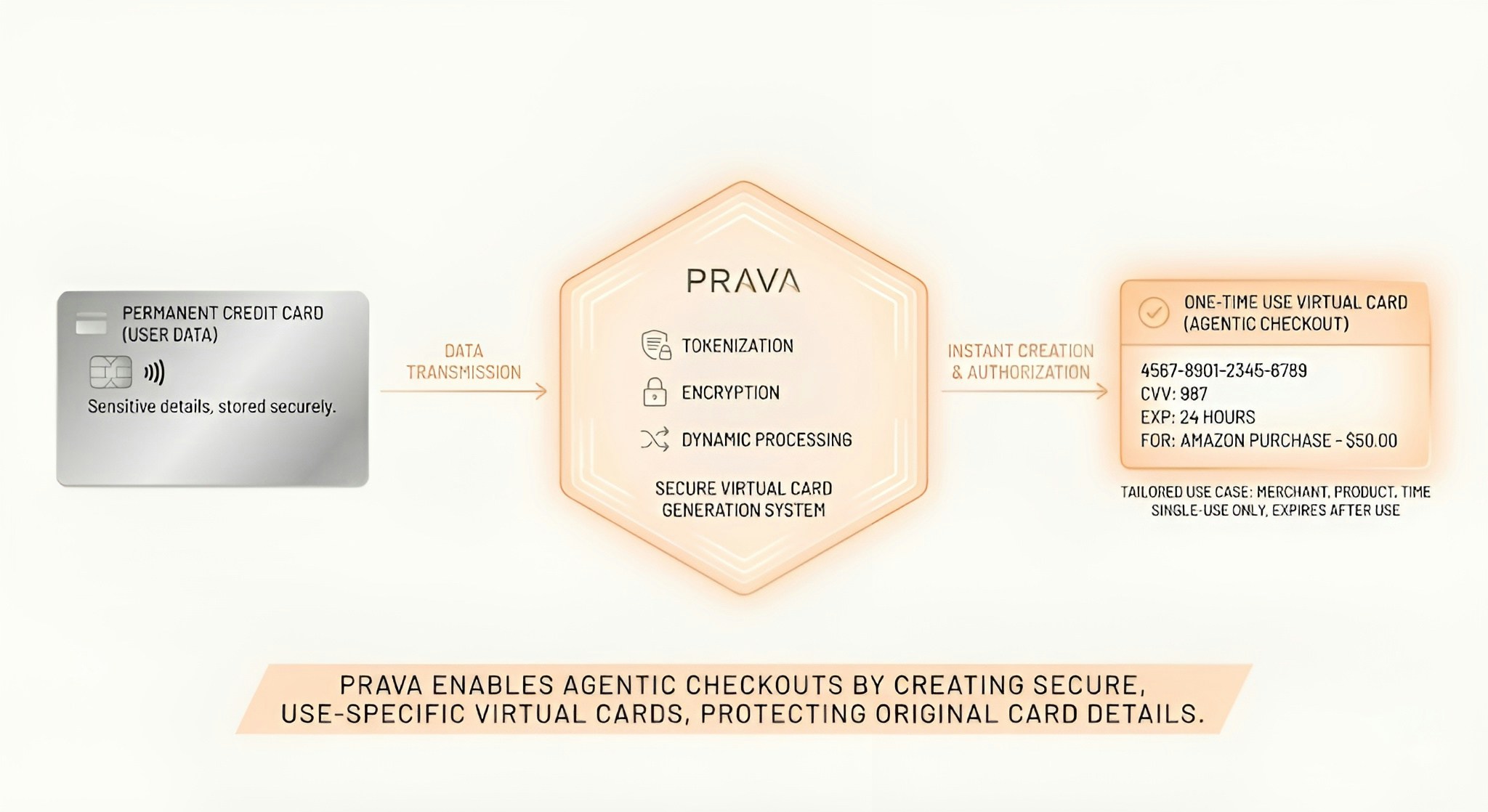

2. The Data Layer (Tokenization)

Users never expose real card numbers to the agent. The card network tokenizes each card. This means the “card” your agent sees is actually a Network Token (DPAN).- Bound to Context: The token is tied to the user, agent, and specific merchant/product.

- One-Time Use: For every checkout, the agent retrieves a fresh tokenized credential plus a single-use dynamic verification value (cryptogram).

3. The Logic Layer (Intent Object)

The Intent Object is the programmatic definition of “what is allowed”. It captures:- Item details: Product IDs, Names.

- Budget: The maximum authenticated decline threshold.

- Quantity: How many items.

- Timing: When the purchase can occur (immediately or automated later).

- Merchant: The specific verified recipient.

4. Security Architecture

- Device-Bound Authentication: Users authenticate instructions with a device-bound passkey (FIDO/WebAuthn). This is set up once per device/card with issuer step-up (e.g., OTP).

- Merchant Verification: Prava validates the merchant to prevent payments to spoofed sites.

- HTTPS Enforcement: Agents can only transact on HTTPS pages with valid certificates and approved domains.

Technical Implementation Flow

Here is the lifecycle of an agentic payment:1. Credential Provisioning

The app collects card details and sends them to Prava. Prava interacts with the Card Network to tokenize the card and returns a secure reference to the app.2. Authentication & Authorization

When an agent needs to pay, the user must authenticate the instruction.- Mechanism: Device-bound Passkey.

- Scope: Required for Create, Update, and Cancel of instructions.

- Result: The Intent is now “Authorized” and ready for execution.

3. Payload Generation

The agent requests the Checkout Payload from Prava for a specific authorized Intent. The Network Returns:- Tokenized Card Number (DPAN)

- Token Expiry (Month/Year)

- Single-use Dynamic Verification Value (Cryptogram)

Note: This set of data effectively acts as a “Single Use Card”.

4. Execution (Checkout)

The agent injects the Checkout Payload into the merchant’s flow.- Supported Modes: Standard guest web checkouts (secure form-fill) & Merchant APIs.

- Security Check: The network enforces merchant and amount controls at authorization using the retrieved credentials.

5. Processing

The transaction proceeds through the standard rails:Merchant -> Acquirer -> Card Network -> Issuer

6. Reconciliation

Agent Publishes Confirmation After checkout submission, the agent publishes confirmation data (status, amounts, products) back to the Prava network. This is critical for:- Reconciliation

- Fraud Controls

- Dispute Handling

Integration Options

A. Full Prava Agentic SDK (Recommended)

Handles the complex orchestration of tokenization, authentication, intent management, and payload injection.B. API-Only Integration

For teams who need granular control, individual endpoints are available for:- Tokenization

- Intent Creation

- Checkout Payload Generation

Getting Access

Prava is currently in restricted rollout.- Onboarding: Fill the form (AI App or Merchant).

- Review: Prava verifies trust & use-case.

- Access: Get API Keys, Sandbox, and Dashboard within 24h.

Why Developers Use Prava

- Zero PCI Scope: No sensitive card data exposure.

- Global Standard: Future-proof infrastructure aligned with EMV/Network standards.

- Universal Compatibility: Works with any merchant (No-code to API-first).

- Developer Experience: Single SDK for complex payment orchestration.